All Categories

Featured

Table of Contents

One more possibility is if the deceased had an existing life insurance policy plan. In such cases, the assigned beneficiary might obtain the life insurance policy earnings and make use of all or a part of it to pay off the mortgage, enabling them to continue to be in the home. mortgage term life. For individuals that have a reverse mortgage, which permits people aged 55 and above to get a mortgage based upon their home equity, the financing rate of interest accumulates with time

Throughout the residency in the home, no settlements are called for. It is essential for people to very carefully intend and think about these variables when it concerns home mortgages in Canada and their effect on the estate and beneficiaries. Seeking advice from legal and financial professionals can aid make sure a smooth change and proper handling of the mortgage after the homeowner's passing.

It is critical to understand the offered choices to ensure the mortgage is effectively dealt with. After the fatality of a property owner, there are numerous choices for home mortgage payment that depend on different elements, consisting of the regards to the home mortgage, the deceased's estate planning, and the desires of the beneficiaries. Below are some usual alternatives:: If several beneficiaries desire to presume the home loan, they can become co-borrowers and proceed making the home mortgage payments.

This choice can provide a clean resolution to the mortgage and distribute the continuing to be funds among the heirs.: If the deceased had a present life insurance policy, the marked recipient might get the life insurance coverage earnings and utilize them to repay the mortgage (mortgage redundancy cover). This can make it possible for the beneficiary to stay in the home without the worry of the home loan

If no one remains to make home loan settlements after the property owner's fatality, the home mortgage lender deserves to confiscate on the home. The effect of repossession can differ depending on the scenario. If an heir is called but does not market the residence or make the home loan settlements, the home loan servicer could initiate a transfer of ownership, and the repossession could drastically harm the non-paying heir's credit.In instances where a home owner passes away without a will or trust fund, the courts will certainly assign an administrator of the estate, usually a close living relative, to distribute the properties and obligations.

Typical Cost Of Mortgage Insurance

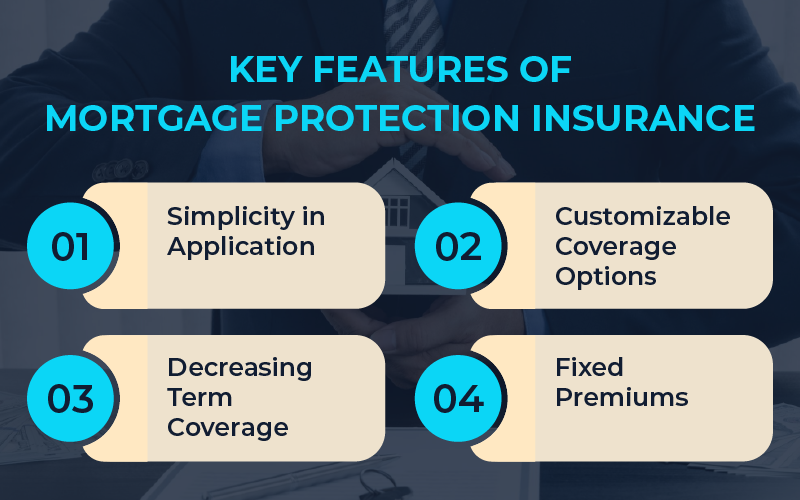

Mortgage security insurance coverage (MPI) is a form of life insurance coverage that is particularly created for people who want to make certain their home mortgage is paid if they pass away or come to be disabled. Often this type of policy is called home mortgage repayment defense insurance policy.

When a bank possesses the big bulk of your home, they are accountable if something occurs to you and you can no more pay. PMI covers their danger in the event of a foreclosure on your home (mortgage protection cost). On the other hand, MPI covers your danger in the occasion you can no more make payments on your home

The quantity of MPI you need will vary depending on your one-of-a-kind circumstance. Some factors you should take into account when taking into consideration MPI are: Your age Your health and wellness Your financial scenario and sources Other kinds of insurance that you have Some individuals might think that if they presently have $200,000 on their home mortgage that they ought to purchase a $200,000 MPI plan.

Mortgage Protection Serious Illness Cover

The brief solution isit depends. The inquiries people have about whether MPI is worth it or not are the exact same inquiries they have concerning acquiring various other kinds of insurance coverage as a whole. For most individuals, a home is our solitary biggest financial obligation. That implies it's mosting likely to be the single biggest economic challenge facing making it through member of the family when an income producer dies.

The combination of anxiety, sadness and changing family members characteristics can create also the very best intentioned people to make expensive mistakes. mortgage repayment cover. MPI resolves that problem. The worth of the MPI plan is straight linked to the equilibrium of your home mortgage, and insurance profits are paid straight to the bank to care for the staying balance

And the biggest and most stressful economic problem encountering the making it through member of the family is solved immediately. If you have wellness problems that have or will certainly produce troubles for you being authorized for routine life insurance policy, such as term or entire life, MPI might be an outstanding option for you. Generally, home mortgage protection insurance coverage do not call for clinical exams.

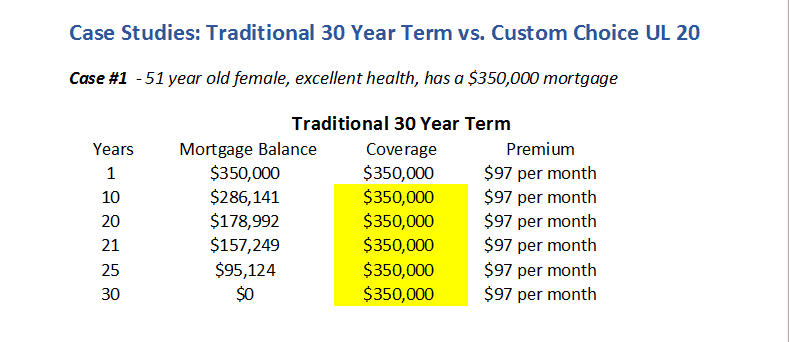

Historically, the amount of insurance policy coverage on MPI plans dropped as the equilibrium on a home mortgage was decreased. Today, the coverage on many MPI policies will continue to be at the exact same degree you acquired. As an example, if your initial mortgage was $150,000 and you bought $150,000 of home mortgage protection life insurance, your recipients will certainly currently receive $150,000 no matter just how much you owe on your home loan - how much is mortgage insurance in california.

If you wish to settle your mortgage early, some insurer will certainly permit you to transform your MPI policy to an additional kind of life insurance policy. This is among the inquiries you could wish to deal with up front if you are thinking about paying off your home early. Prices for home loan security insurance coverage will vary based on a number of things.

Mortgage Protection Florida

An additional factor that will affect the costs quantity is if you purchase an MPI policy that supplies insurance coverage for both you and your partner, giving advantages when either among you dies or becomes disabled. Realize that some business might require your policy to be editioned if you re-finance your home, yet that's generally only the case if you purchased a policy that pays only the balance left on your home mortgage.

What it covers is very slim and plainly specified, depending on the alternatives you pick for your specific plan. If you die, your mortgage is paid off.

For home mortgage defense insurance policy, these forms of extra insurance coverage are added to plans and are understood as living benefit bikers. They enable plan holders to take advantage of their home mortgage protection benefits without passing away. Below's exactly how living benefit motorcyclists can make a home mortgage protection plan better. In instances of, the majority of insurance coverage firms have this as a complimentary advantage.

For instances of, this is usually currently a free living advantage provided by a lot of business, yet each firm specifies advantage payments in different ways. This covers health problems such as cancer, kidney failing, heart strikes, strokes, mental retardation and others. mortgage protection service center. Companies normally pay out in a swelling amount relying on the insured's age and extent of the ailment

In many cases, if you make use of 100% of the permitted funds, after that you utilized 100% of the plan survivor benefit worth. Unlike the majority of life insurance policy policies, purchasing MPI does not need a medical examination a lot of the moment. It is sold without underwriting. This means if you can not obtain term life insurance because of an illness, an assured concern home loan security insurance coverage might be your best option.

Preferably, these need to be individuals you understand and trust who will certainly provide you the very best advice for your situation. No matter of that you determine to check out a plan with, you ought to always shop around, since you do have options - do i have to buy mortgage insurance. In some cases, unexpected fatality insurance is a far better fit. If you do not get term life insurance policy, after that unexpected fatality insurance may make more sense because it's warranty issue and implies you will not undergo medical examinations or underwriting.

Mortgage Insurance Life

Ensure it covers all expenses connected to your mortgage, consisting of interest and payments. Think about these variables when making a decision precisely just how much insurance coverage you think you will require. Ask how quickly the policy will certainly be paid if and when the main revenue earner dies. Your household will be under enough emotional stress without needing to question how much time it may be before you see a payment.

{kind=link}

Latest Posts

Instant Life Funeral Cover

Funeral Home Burial Insurance

Burial Insurance Monthly Cost